Plugging into the future: how are ECVs driving change in Europe?

London, UKJune 17 , 202519 minute read

Farizon Launch seen in Millbrook, United Kingdom on February 25, 2025.

Europe’s commercial transport sector is undergoing a profound shift. Faced with tightening emissions targets, rising fuel costs, and an insatiable appetite for online shopping, policymakers and logistics firms are turning to electric commercial vehicles (ECVs) as a remedy for both environmental concerns and logistical gridlock.

Electric vans now zip through congested cities, while battery-powered lorries prepare to venture ever further across the continent’s motorways. Governments are pouring public funds into charging infrastructure and tightening the regulatory screws on gasoline and diesel. Manufacturers, for their part, are racing to electrify their line-ups, hoping to stay ahead of both rivals and regulations.

Light Commercial Vehicles (LCVs) – mainly urban delivery vans – are leading the way. But the electric revolution is not confined to the city: momentum is growing in the heavy-duty segment, too, as range improves and costs fall. What was once niche, is on track to become the norm.

How fast is the electric commercial vehicle market growing?

Europe’s appetite for LCVs is increasing every year. In 2023, the continent snapped up 1.9 million of them – 1.7 million of which were vans. Nearly all fell below the 3.5-ton mark, accounting for 99.1% of sales. By 2032, annual sales are projected to hit 2.4 million, implying a steady compound growth rate of 2.9%.[1]

These are just the new arrivals. On the road, the total LCV fleet is far larger. Some 30.1 million vans trundle across the EU, with half concentrated in just three countries: France (6.5 million), Italy (4.5 million) and Spain (4 million).[2] Medium and heavy commercial vehicles are fewer – about 6 million – but similarly clustered, with Italy, Germany and Poland together accounting for almost half.

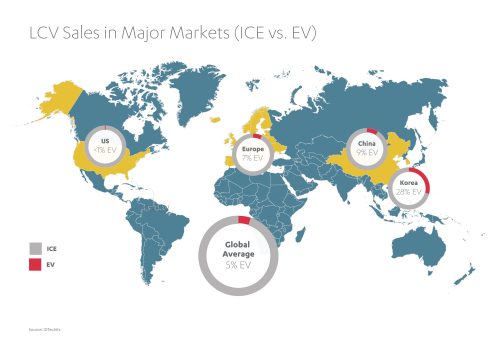

However, Europe’s roads are still dominated by diesel. Over 90% of LCVs and 96.4% of trucks guzzle the stuff, while battery-electric vans account for just 1.1% of the total, and zero-emissions trucks barely register at 0.1%.[3]

Source: IDTechEx

However, the pace of change is accelerating.

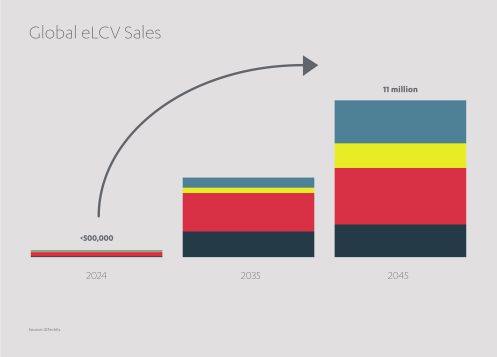

Sales of electric LCVs surged by 60% in 2023 – outpacing the global average – and reached nearly 150,000 units.[4] By 2032, electric vehicles are expected to make up 60% of Europe’s LCV sales.[5] That creates a lucrative opportunity for manufacturers and distributors. The market is forecast to balloon from US$ 7.5 billion in 2023 to US$ 29.1 billion by 2029, a compound annual growth rate of over 25%.[6] The age of the electric van is fast approaching.

Source: IDTechEx

Where are electric commercial vehicles most popular?

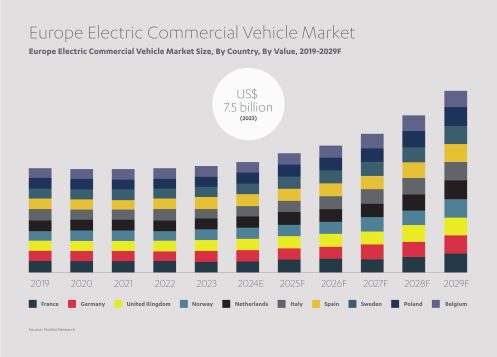

The European electric commercial vehicle is in good health – pulling ahead of the global average. In 2023, France emerged as a European leader in eLCVs, driven by strong government incentives, environmental policies, and expanding charging infrastructure. National and local support – including subsidies, tax breaks, and low-emission zones – has encouraged businesses, especially SMEs, to transition to electric fleets. As battery technology improves and costs fall, France is expected to remain at the forefront of eLCV adoption in Europe.[7]

Source: TechSci Research

What are the main electric vehicle propulsion types? The European electric commercial vehicle market comprises four main modes of propulsion: Battery Electric Vehicles (BEV) – Fully electric, zero-emission vehicles powered by batteries. Ideal for urban deliveries due to short-range operation, low maintenance, and environmental benefits.Hybrid Electric Vehicles (HEV) – Combine an internal combustion engine with an electric motor. Recharge internally (no plug-in needed) and offer better fuel efficiency. Suitable for long-range operations where charging infrastructure is limited.Plug-in Hybrid Electric Vehicles (PHEV) – Similar to HEVs but can be externally charged. Operate electrically for short trips and switch to fuel for longer distances. Offer flexibility for businesses balancing sustainability with range requirements.Fuel Cell Electric Vehicles (FCEV) – Use hydrogen to generate electricity, producing only water vapor as emissions. Offer long range and quick refueling, suitable for heavy-duty and long-distance transport. Their growth depends on expanding the hydrogen infrastructure and access to green hydrogen.

What’s driving growth in the European electrical commercial vehicle market?

At the heart of the market momentum seem to be three core considerations:

Sustainability & savvy branding: eLCVs produce zero tailpipe emissions, making them a vital alternative to traditional diesel-powered fleets that are seen to do relatively more harm the environment and impact local air quality. Businesses across sectors – particularly logistics, retail, and last-mile delivery – are integrating electric vehicles into their fleets to align with their sustainability goals and societal sentiment. It’s not only about regulatory compliance or emissions reduction; it’s sound business sense. Greener fleets appeal to environmentally conscious consumers and investors.

Cheaper in the long run? Expensive and volatile fuel prices encourage fleet operators to seek alternatives. EVs avoid these fluctuating operating fuel costs and also with fewer moving/mechanical parts, which makes them cheaper to run and maintain than traditional internal combustion engine (ICE) vehicles – offering long-term savings and total cost of ownership.[8]

Policy, pressure & incentives: Governments across Europe are tightening the regulatory noose on carbon-heavy transport. In line with the Paris Agreement[9], many have committed to ambitious emissions targets, nudging businesses toward cleaner fleets through a mix of carrots and sticks. Subsidies, tax credits, and exemptions from road charges sweeten the deal, while emissions caps and low-emission zones increase the pressure.

The EU’s “Green Deal” and its “Fit for 55” package – aimed at slashing greenhouse gas emissions by 55% by 2030 – are setting the pace.[10] Urban low-emission zones, already common across Europe, are expected to proliferate under the EU’s Climate-Neutral and Smart Cities initiative. Several countries, including Britain, Norway, Denmark, and Spain, are going further by planning zero-emission zones in their largest cities.

The trend dovetails neatly with the logistics sector’s shift toward electric vehicles for last-mile delivery. As urban centers grow more congested and emissions regulations tighten, the appeal of nimble, cost-effective electric vans that can zip through clean-air zones is growing.

National and supranational funding also play a major role. In December 2024, French fleet management and leasing company Ayvens signed a landmark €700 million financing agreement with the European Investment Bank (EIB) to expand its fleet of eLCVs across Europe. This includes a €350 million green loan from the EIB – the first of its kind for eLCVs – and a matching co-investment by Ayvens. The funding will support the rollout of 19,000 eLCVs over the next three years, mainly in Germany, France, Italy, and the Netherlands, as part of an EU-backed climate action initiative.[11]

Heavy-duty vehicles are next. The EU wants a 90% cut in carbon emissions from trucks by 2040. The UK is plowing US$ 250 million into a pilot program that will put 370 zero-emission HGVs and nearly 60 charging or refueling stations on the road.[12] A full ban on fossil-fuel trucks looms, with 2035 the target in the EU and 2030 under discussion in the UK.[13] International coalitions – from EV100+ to the European Clean Trucking Alliance – are also pushing for swifter fleet electrification. For diesel, the end of the road is approaching.

What are the latest innovations in electric commercial vehicle technology?

Better batteries: Modern batteries have significantly enhanced the performance and affordability of eLCVs. Their longer ranges, longer lifespans, faster charging times, and lower maintenance costs make them a more viable alternative to traditional ICE vehicles. Between 2015 and 2023, the average range of new eLCVs increased by 55%.[14] In 2015, popular models like the Nissan e-NV200 and Renault Kangoo BEV offered ranges of around 170 km. By 2023, the Hyundai Porter and Ford E-Transit were reaching between 210 km and 260 km. Despite these gains, many fleet operators continue to call for more accurate and transparent range labeling as they scale up their electric vehicle deployments.[15]

Smarter tech solutions: The eLCV market is seeing rapid adoption of smart technologies such as telematics, fleet management software, and autonomous driving features. These tools help fleet operators optimize routes, monitor battery health, manage maintenance, and boost overall efficiency. Real-time data insights also contribute to lower operational costs and better service delivery. These technologies will continue to enhance the performance and appeal of eLCVs for businesses.

Vehicle-to-Grid (V2G) technology: this technology enables electric vehicles to feed stored energy back into the power grid. This helps to balance supply and demand, particularly during peak periods. It also enables fleet operators to turn vehicles into mobile energy assets, potentially earning revenue by selling excess energy. As electric vehicle adoption accelerates, V2G is set to play a growing role in smart energy management.

How are OEMs responding to rising demand in Europe for electric commercial vehicles?

Stellantis dominates the European LCV market, accounting for one-third of all sales, followed by Ford (18%), Renault-Nissan (15%), and German automakers Volkswagen and Mercedes-Benz (combined 21.5%).[16] Several Chinese brands are selling LCVs in Europe, with notable players like BYD, SAIC Motor (MG), Geely, and their subsidiaries making significant inroads.

As core EV technologies mature, virtually all major LCV manufacturers offer or are developing electric versions of their top models. Over 100 eLCV models from global OEMs like Renault, Ford, Hyundai, and Geely reflect evolving trends in design, batteries, and motors.

Stellantis recently revamped its electric van range, presenting twelve new models in 2023. Meanwhile, Mercedes-Benz launched the eCitan, a fully electric small van for inner-city delivery and service operations. Renault plans to launch three new vans in 2026, including the next-generation Trafic, the Estafette, and the Goelette E-Tech.

Chinese OEMs lead in battery-electric heavy-duty vehicle (HDV) models, producing 430 – mostly buses for urban transport (40%). In contrast, European OEMs offer fewer models (~120) but with a more balanced spread across segments, including the highest share of heavy-duty trucks (>20%).[17] Europe also produces a notable share of niche electric HDVs, like refuse trucks, which are already cost-competitive with fossil fuel versions.[18] While Europe matched China in the number of HDV OEMs by 2023 (36), the market is dominated by established players, leaving limited room for new entrants.[19]

What is Jameel Motors doing to support the growth of electric commercial vehicles?

In September 2024, Jameel Motors (International) announced a major global distribution agreement with Geely Farizon, covering 11 countries with a combined population of over 450 million. The deal will see Jameel Motors distribute Geely’s Farizon Auto full range of New-Energy Commercial Vehicles (NECV) – including electric, and later potentially hybrid, hydrogen, and methanol models – marking new market entries for the Chinese manufacturer. This collaboration leverages Jameel Motors’ 70 years of automotive experience and supports its strategy to expand and diversify into sustainable mobility solutions globally. As part of the deal, Jameel Motors launched the Geely Farizon SV electric van in the UK, Australia and the UAE in 2025, marking a new market entry for both companies.

The SV is a large, “born-electric” panel van developed specifically for European fleets, featuring advanced technologies like a dual-redundancy drive-by-wire system and cell-to-pack battery design, which improve range, performance, safety, and cargo capacity. The van is available in multiple lengths, heights, and battery sizes. Jameel Motors UK has partnered with major UK industry players including DHL and the AA, bolstering confidence in the new model SV.

Adding to this the Farizon H9E electric medium truck has been introduced into the UAE and Australia. Jameel Motors has also announced it will become the exclusive distributor of GAC’s new energy vehicles in Poland, introducing advanced electric passenger cars from GAC’s Aion and Hyptec brands. It is also partnering with Geely Auto in Poland to distribute its advanced line-up of NEVs, offering Polish consumers access to innovative, high-tech, and sustainable vehicles from China’s leading automakers.

How is EV battery technology developing in Europe?

EVs aren’t going anywhere without the right batteries. Fortunately, Europe is well placed in this regard, from manufacturing and continuing innovation to end-of-life services.

Over the past five years, significant investment in mining and refining has led to a surplus in key minerals like cobalt, nickel, and lithium, keeping current supply ahead of demand and lowering battery and mineral prices. Most EV battery demand in Europe is met through domestic or regional production, though Europe relies on imports for over 20% of its needs.[20] China remains the top EV battery exporter. In 2023 Europe produced 110 GWh of batteries and 2.5 million EVs, with Poland and Hungary leading battery output. According to estimates, the EU’s Net Zero Industry Act and relaxed state aid rules have attracted enough investment to meet the EU’s 2030 electrification targets.[21]

Lithium iron phosphate (LFP) batteries – more stable and with a longer lifespan – have rapidly gained traction, accounting for over 40% of global EV battery demand by capacity in 2023, more than double their 2020 share. While China leads LFP production and adoption (used in two-thirds of its EVs), Europe and the US still favor high-nickel chemistries, with LFP adoption below 10%.[22]

Innovations like cell-to-pack and cell-to-chassis designs are improving LFP performance while manufacturing advancements – such as multi-layer electrodes – support ultra-fast charging. There’s also a push to increase manganese content in LFP and NMC batteries to enhance energy density or reduce costs.

Meanwhile, sodium-ion batteries are being explored as a low-cost, low-mineral alternative. Though initially developed in the U.S. and Europe, China now dominates sodium-ion manufacturing, with capacity roughly ten times that of the rest of the world combined.[23]

What are the main challenges to electric commercial vehicle uptake?

Although general confidence is high, achieving the promised future of commercial EVs will require addressing a few key hurdles.

Affordability: Electric vehicles may be quietly revolutionizing logistics, but their sticker price still deters many fleet operators, particularly small and medium-sized enterprises (SMEs). Though cheaper to run and maintain than their diesel counterparts, eLCVs remain burdened by hefty upfront costs, largely driven by the price of batteries. Lower resale values further undermine the business case for some buyers, making the total cost of ownership less compelling than hoped. The gap is narrowing, though. As battery prices fall, economies of scale kick in, and public subsidies sweeten the deal, analysts believe price and resale parity with internal combustion vehicles is within reach. When that happens – soon, by most estimates – eLCVs will no longer be an expensive luxury, but a pragmatic choice for a far broader swathe of Europe’s business community.

Limited vehicle variety: Choice, for now, remains the Achilles’ heel of electric commercial vehicles. While the number of electric vans and trucks has grown, the variety on offer still pales in comparison to the vast and specialized array of ICE models. Today’s electric alternatives may fall short for fleet operators with specific operational needs, be it unusual cargo volumes, bespoke configurations, or sector-specific demands.

Battery lifespan and performance: Though battery technology has made impressive strides, doubts about durability continue to dog the eLCV sector. Over time, even the best batteries degrade – reducing range, cutting performance, and raising operational costs. For fleet managers already wary of capital expenditure, the prospect of costly mid-life battery replacements could be enough to stall investment. Improving battery durability and advancing recycling solutions are essential to ensuring the long-term viability and appeal of eLCVs.

Energy supply and charging infrastructure: As the EV fleet swells across Europe, so too does the strain on the continent’s energy systems. Power grids designed for conventional demands are facing an electrified future where large commercial fleets require rapid, round-the-clock charging. Peak-hour consumption spikes risk overwhelming infrastructure not built for such loads, and upgrading the grid will be costly and time-consuming. For fleet operators, the challenge is not just where to plug in, but when.

Infrastructure is catching up – slowly. Public charging remains patchy, especially outside major cities. In rural or suburban zones, the scarcity of fast-charging stations continues to fuel “range anxiety”, deterring many businesses from switching to battery-powered commercial vehicles. To plug the gap, the EU has turned to regulation. Under the Alternative Fuels Infrastructure Regulation (AFIR), finalized in late 2023, member states must ensure that fast chargers for light-duty vehicles are available every 60km along key transport routes by 2030. By the end of 2025, at least one ultra-fast charger (350kW minimum) must be installed per station for heavy-duty vehicles (HDVs).[24]

For its part, the UK has scrapped consumer EV subsidies but doubled down on charging infrastructure, installing over 53,600 public chargers in 2023 alone, with a goal of 300,000 by decade’s end.[25] Germany, meanwhile, is rolling out 350 charging hubs along federal motorways.[26] But beyond rollout, regulators are now turning their attention to improving payment interoperability, charger uptime, and equitable access.

High-powered charging – particularly for electric heavy trucks – poses fresh headaches. The energy intensity of fast charging risks destabilizing local grids, particularly in industrial zones where multiple megawatt-scale chargers may operate simultaneously. Some governments, such as the Netherlands, are piloting strategies to mitigate these spikes, including the co-location of renewable energy generation and on-site battery storage.[27] More radical solutions – like electric road systems or battery swapping – are being tested to ease the load and accelerate turnaround times.[28]

Unless the infrastructure keeps pace, the promise of emissions-free logistics could stall in a queue for the next available plug.

What is the future for electric commercial vehicles in Europe?

Europe’s ECV sector is no longer an experiment but an inevitability. Electric vans and trucks are now carving a credible path through city centers and logistics corridors alike. Policymakers have laid the groundwork with aggressive emissions targets, generous subsidies, and tightening urban access rules. Manufacturers, prodded by regulation and market demand are delivering ever more capable and cost-competitive models. And investors, sensing an inflection point, are flooding the sector with capital, from batteries to infrastructure.

However, the road to electrification remains somewhat bumpy. Charging networks are still patchy, especially outside metropolitan centers. Battery supply chains are stretched, and energy grids creak under growing demand. Cost and range anxieties still linger, particularly among smaller fleet operators. But these barriers are eroding. Technology is improving, economies of scale are taking hold, and the policy momentum is unmistakable. For now, diesel may still rule the road – but Europe’s freight future, it seems, will soon hum rather than roar.

Five fast facts on the electric commercial vehicle market in Europe

How many electric LCVs were sold in Europe in 2023? Nearly 150,000 electric light commercial vehicles (eLCVs) were sold in Europe in 2023, with sales rising 60% compared to the previous year.

What percentage of Europe’s LCV sales are expected to be electric by 2032? eLCVs are expected to make up 60% of Europe’s light commercial vehicle sales by 2032.

What is the EU’s target for reducing carbon emissions from trucks by 2040? The EU wants a 90% cut in carbon emissions from trucks by 2040.

How has the range of new eLCVs improved in recent years? Between 2015 and 2023, the average range of new eLCVs increased by 55%, with some newer models reaching between 210 km and 260 km.

What infrastructure requirement has the EU mandated for electric vehicles along key transport routes? Under the Alternative Fuels Infrastructure Regulation (AFIR), EU member states must ensure that fast chargers for light-duty vehicles are available every 60km along key transport routes by 2030.

Mumbai, IndiaAugust 27 , 2025

Mumbai, IndiaAugust 27 , 2025 15 minute read

15 minute read